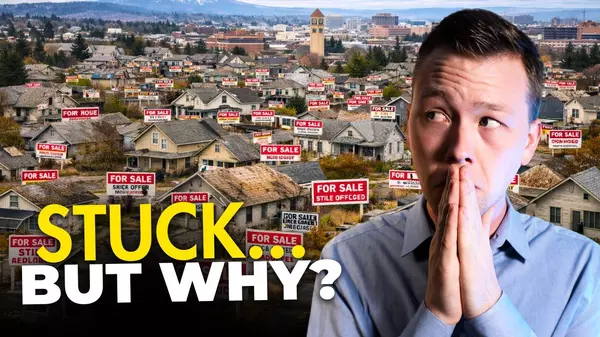

Should I Rent or Buy in Today's Housing Market? Here’s How to Decide

Buying a home is a significant milestone and life goal for many individuals. While the common belief is that renting is wasting money, and homeownership is an investment that builds equity, the truth is more nuanced. Several factors, including personal finances, lifestyle, goals, location, and the e

Keys to Success for First-Time Homebuyers

Purchasing your first home is an exhilarating decision and a significant milestone that can positively impact your life. However, recent years have presented challenges for first-time homebuyers, including tight inventory, rising home prices, increasing rents, and high student debt loads, resulting

Is the Spokane Real Estate Market Hot or Not?

Spokane's real estate market has been through significant changes in recent years, experiencing both price drops and subsequent recovery. This blog post aims to provide a comprehensive overview of the top five neighborhoods in Spokane that have experienced price drops over the last 12 months. Addi

Categories

- All Blogs (907)

- Airway Heights (5)

- Audubon/Downriver (4)

- Balboa/South Indian Trail (5)

- Bemiss (3)

- Browne's Addition (3)

- Buying Your Home in Spokane (207)

- Cheney (3)

- Chief Garry Park (3)

- Cliff-Cannon (3)

- Colbert (1)

- Comstock (4)

- Cost of Living in Spokane (1)

- Dishman (3)

- Downtown Spokane (1)

- Driving Tours (1)

- East Central (3)

- Emerson/Garfield (3)

- Five Mile Prairie (5)

- Grandview/Thorpe (3)

- Greenacres (3)

- Hillyard (3)

- Home Improvement (8)

- Home Prices (5)

- Housing Inventory (6)

- Housing Market (133)

- Housing Market Update (2)

- Instagram Videos (2)

- Interest Rates (24)

- Job Market in Spokane (3)

- Know Spokane (605)

- Latah Valley (5)

- Liberty Lake (8)

- Lincoln Heights (4)

- Living in Spokane (2)

- Logan (3)

- Manito-Cannon Hill (3)

- Medical Lake (4)

- Minnehaha (3)

- Moran Prairie (3)

- Mortgage (26)

- Moving out of Spokane (3)

- Moving to Spokane (143)

- Nevada/Lidgerwood (3)

- New Construction Homes in Spokane (1)

- New Construction Opportunities (3)

- North Hill (3)

- North Indian Trail (4)

- Northwest (3)

- Opportunity (3)

- Peaceful Valley (3)

- Riverside (3)

- Rockwood (4)

- Selling Your Spokane Home (163)

- Shiloh Hills (3)

- Southgate (3)

- Spokane Events (444)

- Spokane Neighborhoods (51)

- Spokane Restaurants/Food Places (24)

- Spokane Schools (12)

- Spokane Valley (14)

- Suncrest (1)

- Things to Do in Spokane (457)

- Veradale (3)

- West Central (3)

- West Hills (3)

- Whitman (3)

- Youtube Videos (49)

Recent Posts